The freelance economy is booming. In 2023, 71% of freelancers relied on independent work as their main source of income, a significant increase from previous years. This shift signifies that for a growing majority, freelancing isn’t just a side hustle; it’s their primary career path, generating an estimated $1.5 trillion in earnings in the U.S. alone in 2024. While this independence offers unparalleled freedom and flexibility, it also introduces a unique financial challenge: the notorious “feast and famine” cycle. Irregular income can create stress, hinder planning, and impede long term growth. This guide provides freelancers with actionable strategies and systems for proactive money management, ensuring financial stability and enabling sustained success.

The Freelance Roller Coaster: Understanding the Challenge

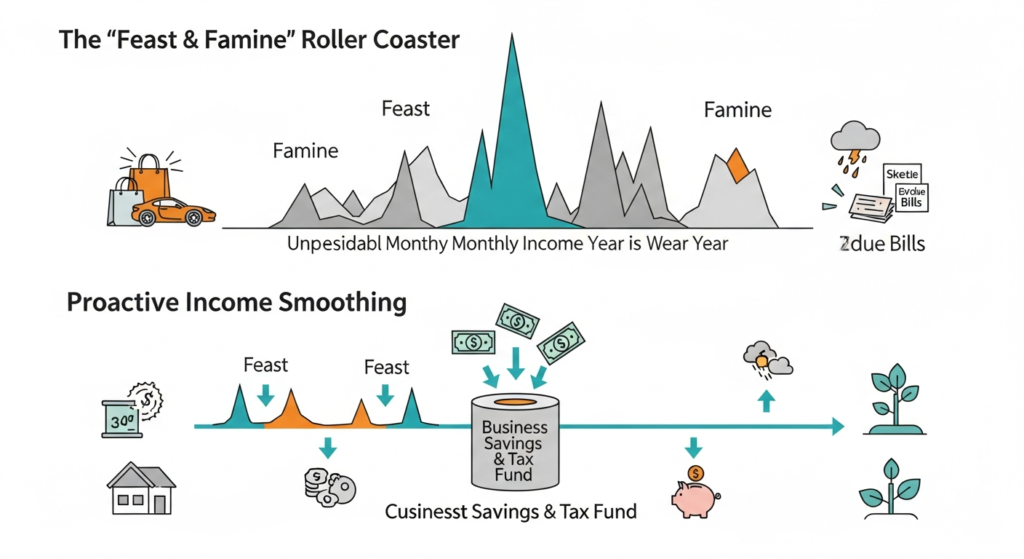

Acknowledging the “Feast and Famine” Cycle of Freelancing

The inherent nature of freelancing often leads to unpredictable income flows. Project based work, seasonal client demands, and the ebb and flow of business development mean that periods of high earnings can be followed by leaner times. This irregularity is not a sign of poor performance but rather a characteristic of the self-employed landscape. Many freelancers find that 68% of independent professionals report that the unpredictable nature of freelance work can make it difficult to maintain a consistent income stream. Understanding this cycle is the first step toward managing it effectively.

The Emotional and Financial Impact of Income Peaks and Valleys

The “feast and famine” cycle has tangible consequences. During peak earning periods, there’s a temptation to overspend, assuming the good times will last. Conversely, during lulls, anxiety can set in, impacting decision making and potentially leading to taking on undesirable projects out of necessity. This financial instability can contribute to significant stress, affecting mental well being, relationships, and overall productivity. The inability to rely on a steady income makes long term planning, such as saving for retirement or

Why Proactive Income Smoothing is Essential for Self-Employment and Gig Workers

Proactive income smoothing isn’t just about surviving the downturns; it’s about thriving. By implementing robust financial management strategies, freelancers can transform unpredictable cash flow into a controllable asset. This proactive approach fosters financial stability, allowing for consistent business reinvestment, personal growth, and a reduction in financial stress. It shifts the freelancer from a reactive position, scrambling to cover expenses, to a strategic one, confidently navigating their career path and achieving their long term goals.

Laying the Foundation: Mastering Your Freelance Finances

Separating Personal and Business Finances

The most fundamental step for any freelancer is to establish a clear separation between personal and business finances. This means opening dedicated business bank accounts and credit cards. This practice is crucial for accurate income and expense tracking, simplifies tax preparation, and presents a more professional image to clients. Without this separation, it becomes nearly impossible to understand your true business cash flow, profitability, and the actual amount available for personal living expenses.

Comprehensive Tracking: Your Financial GPS for Cash Flow

Effective money management hinges on meticulous tracking of all financial transactions. This includes every invoice sent, every payment received, and every business expense incurred. Utilizing accounting software or detailed spreadsheets can provide a real-time overview of your cash flow. Understanding your incoming income and outgoing expenses allows for informed decision making, helps identify areas of overspending, and provides the data necessary for accurate budgeting and forecasting. This granular view acts as your financial GPS, guiding you through the complexities of freelance finances.

Crafting Your Budget: The Cornerstone of Stability

A budget is more than just a spending plan; it’s a roadmap to financial stability. For freelancers, budgeting requires an adaptive approach that accounts for fluctuating income. The first step is understanding your essential living costs.

Begin by identifying your non negotiable expenses, such as rent or mortgage, utilities, groceries, and healthcare. These are the costs you absolutely need to cover every month. Once you’ve got a clear understanding of your baseline expenses, calculate your average monthly spend over the past several months to get a realistic view of your financial needs.

Identifying Your Baseline: What You Truly Need to Live On

Before you can effectively manage your income, you must know your absolute minimum living expenses. This involves detailing all non negotiable costs: housing, utilities, food, essential transportation, and insurance premiums. This baseline figure is critical for determining how much income you need to consistently generate to maintain your lifestyle, even during leaner months. Knowing this number provides a crucial anchor for your budgeting efforts.

Proactive Strategies for Smoothing Income Flow

Paying Yourself a Consistent “Salary”

One of the most effective strategies for taming income volatility is to pay yourself a consistent “salary” from your business income. During periods of high earnings, instead of spending the surplus, allocate a predetermined amount to a separate business checking account from which you draw your regular “paycheck.” This provides a sense of predictability and psychological comfort, mimicking the stability of traditional employment and reducing the urge to overspend during peak times.

Building an Income Buffer: Your Strategic Cash Flow Account

Beyond your personal emergency fund, a dedicated business income buffer is invaluable. This is a separate savings account designed to absorb short term fluctuations in cash flow. When income exceeds your “salary” draw and essential business expenses, transfer the excess into this buffer. During slower months, you can draw from this account to supplement your income, ensuring that your consistent “salary” payments can continue without interruption. This system acts as a shock absorber for your business finances.

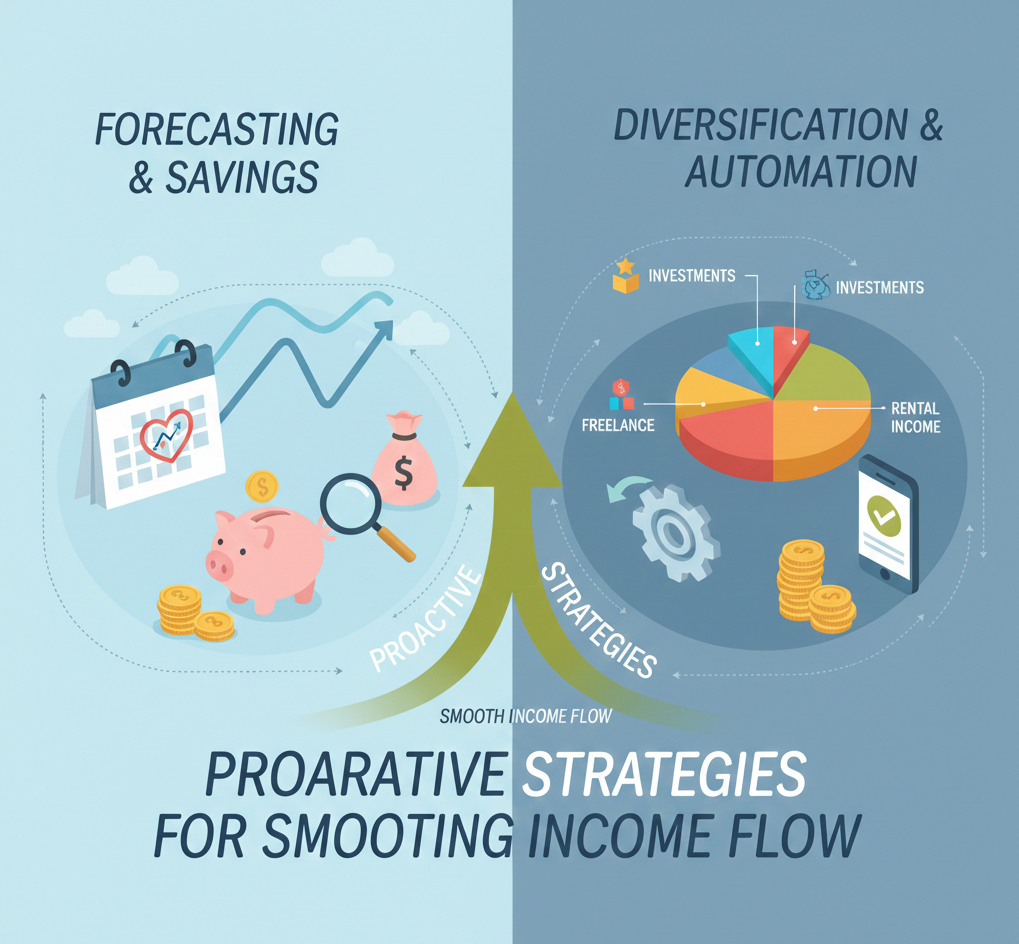

Strategic Cash Flow Planning and Forecasting

Regularly forecasting your income and expenses is a powerful tactic for proactive management. By analyzing past project cycles, upcoming contracts, and potential leads, you can project your likely cash flow for the next few months. This forecasting allows you to anticipate potential shortfalls or surpluses, enabling you to adjust your spending, plan for tax payments, or strategically reinvest during anticipated high earning periods. This forward looking approach is key to maintaining steady income.

Diversifying Your Income Streams

Relying on a single client or type of project creates significant risk. Diversifying your income streams is a vital strategy for building resilience. This could involve offering a broader range of services, developing passive income sources (like online courses, affiliate marketing, selling digital template or an e-book), or working with multiple clients across different industries. By spreading your income sources, you reduce your vulnerability to any single client’s financial issues or shifts in market demand, contributing to a more steady overall income. Many freelancers are already reinvesting a significant portion of their earnings back into their business; 94% of independent professionals spent some of their freelancing revenues on their business in 2023, with an average reinvestment rate of 32%, indicating a focus on growth and stability.

The “Brakes On, Accelerator Pedal” Tactic in Practice

This tactic involves intelligently managing spending based on your cash flow. During slower periods or when building your income buffer, apply the “brakes” by reducing non-essential business and personal spending. Conversely, during peak earning times, instead of simply increasing personal consumption, use the “accelerator pedal” to strategically reinvest in your business. This could mean investing in new equipment, professional development, marketing efforts, or expanding your service offerings. This disciplined approach ensures that high-earning periods fuel future growth and stability.

Think of your spending like driving a car through a hilly landscape.

| Phase | Action | Example |

| The Famine (Uphill) | Hit the Brakes | Cancel unused SaaS subscriptions; cook at home; pause non-essential marketing spend. |

| The Feast (Downhill) | Hit the Accelerator | Buy that new laptop; invest in a $500 certification; run LinkedIn ads to find the next client. |

Building Your Financial Safety Net and Future Growth

The Non-Negotiable Emergency Fund

An emergency fund is distinct from your business income buffer. This personal savings account is your ultimate safety net, designed to cover unexpected personal crises such as medical emergencies, major home repairs, or extended periods of unemployment due to unforeseen circumstances. Aim to save 3-6 months of essential living expenses in a readily accessible, high yield savings account. This fund provides crucial peace of mind, allowing you to weather genuine crises without derailing your business or personal finances.

Planning for Taxes: Eliminating Surprises

For freelancers, taxes are a significant and often unpredictable expense. Failing to plan can lead to severe financial strain. It’s imperative to set aside a portion of every payment received specifically for taxes. Many jurisdictions require quarterly taxes payments to avoid penalties. Automating this process by regularly transferring a percentage of your income into a dedicated tax savings account ensures you meet your obligations and prevents the stress of a large, unexpected tax bill. This proactive management is crucial for long term financial stability.

Investing in Your Long Term Financial Stability and Growth

Once your essential finances, emergency fund, and tax obligations are managed, focus on long-term growth. This involves investing surplus income strategically. Consider retirement accounts like SEP IRAs or Solo 401(k)s, which offer tax advantages for self-employed individuals. Beyond retirement, explore investment opportunities that align with your risk tolerance and financial goals. Consistent investment, even small amounts, is key to building wealth and securing your future financial stability.

Leveraging Technology and Systems for Automated Management

Smart Budgeting and Expense Tracking Tools

Modern technology offers powerful solutions for freelancer money management. Numerous apps and software platforms are designed to streamline budgeting, expense tracking, and cash flow analysis. Tools like QuickBooks Self-Employed, Xero, or even simpler applications like Mint can automate many tedious tasks, providing clear financial dashboards and helping you stay organized. Implementing these systems reduces manual effort and improves accuracy.

Streamlining Invoicing and Payment Collection Systems

Efficient invoicing and prompt payment collection are vital for maintaining healthy cash flow. Utilize invoicing software that allows for professional customization, automated reminders for overdue payments, and multiple payment options for clients. Clear payment terms upfront, consistent follow-up, and streamlined systems significantly reduce the time and stress associated with chasing payments, ensuring your income arrives as expected.

Automating Savings and Investment Transfers

The most effective way to ensure consistent saving and investing is through automation. Set up recurring automatic transfers from your business checking account to your various savings accounts, including your emergency fund, income buffer, and investment accounts. This tactic removes the temptation to spend the money and ensures that your savings goals are met consistently, regardless of your immediate financial feelings or the presence of high income periods. This builds financial discipline effortlessly.

The Power of Consistent Bookkeeping and Financial Systems

Building and adhering to consistent bookkeeping systems is not a chore; it’s the bedrock of intelligent financial management. Regularly dedicating time each week or month to review your transactions, update your records, and reconcile your accounts is essential. This disciplined approach ensures your financial data is accurate, provides valuable insights into your business performance, and makes tax preparation significantly less daunting. Strong systems lead to robust financial stability.

The Mindset Shift: Embracing Financial Resilience

Moving from Reactive to Proactive Money Management

The core of smoothing out income peaks and valleys lies in a fundamental mindset shift. Instead of reacting to financial emergencies as they arise, adopt a proactive stance. This involves consistently applying the strategies discussed: budgeting, saving, forecasting, and strategic investing. By building robust systems and habits, you gain control over your finances, reducing anxiety and empowering yourself to make better long term decisions.

Developing Financial Discipline and Education

Financial resilience is cultivated through discipline and continuous learning. Make it a priority to educate yourself on personal finance and freelancing management. Read books, take online courses, and stay informed about financial best practices. Apply this knowledge with discipline, sticking to your budget, consistently saving, and making thoughtful financial choices. This commitment to financial education and discipline is a powerful driver of sustained growth.

Managing Stress and Maintaining Well-being Amidst Fluctuations

The emotional toll of unpredictable income can be significant. Implementing sound financial management strategies directly contributes to reduced stress. Knowing you have an emergency fund, a consistent salary, and a plan for taxes provides immense psychological relief. Prioritize self-care, maintain a healthy work-life balance, and seek support from peers or professionals when needed. Financial well-being is intrinsically linked to overall mental and physical health.

Celebrating Small Wins and Committing to the Long Haul

Achieving financial stability as a freelancer is a marathon, not a sprint. Acknowledge and celebrate your progress, whether it’s hitting a savings goal, successfully navigating a lean month, or landing a significant client. These small wins build momentum and reinforce your commitment to your financial plan. Stay focused on the long-term benefits of consistent effort: steady income, professional growth, and the ultimate freedom that comes with mastering your finances.

Conclusion

Navigating the freelance landscape requires more than just talent; it demands astute financial management. By understanding the inherent income fluctuations of freelancing, laying a strong foundation of separated finances and diligent tracking, and implementing proactive strategies like consistent salary payments, income buffers, and diversified income streams, freelancers can effectively smooth out the peaks and valleys. Building a robust emergency fund, diligently planning for taxes, and leveraging technology for automated systems further solidifies financial stability. Ultimately, the journey from reactive crisis management to proactive money management is an empowering one, fostering resilience, enabling sustainable growth, and paving the way for long-term financial freedom and peace of mind. Start implementing these tactics today to build a more steady and prosperous freelance career.